In the second half of 2026, High‑Risk payments are shaped by a small set of structural shifts rather than dozens of buzzwords. For iGaming, Forex, and other emerging markets, these shifts affect how businesses design their payment infrastructure, choose a payment partner, and plan next GEO launches.

Here are our TOP-3 payment and regulation trends for H2 2026.

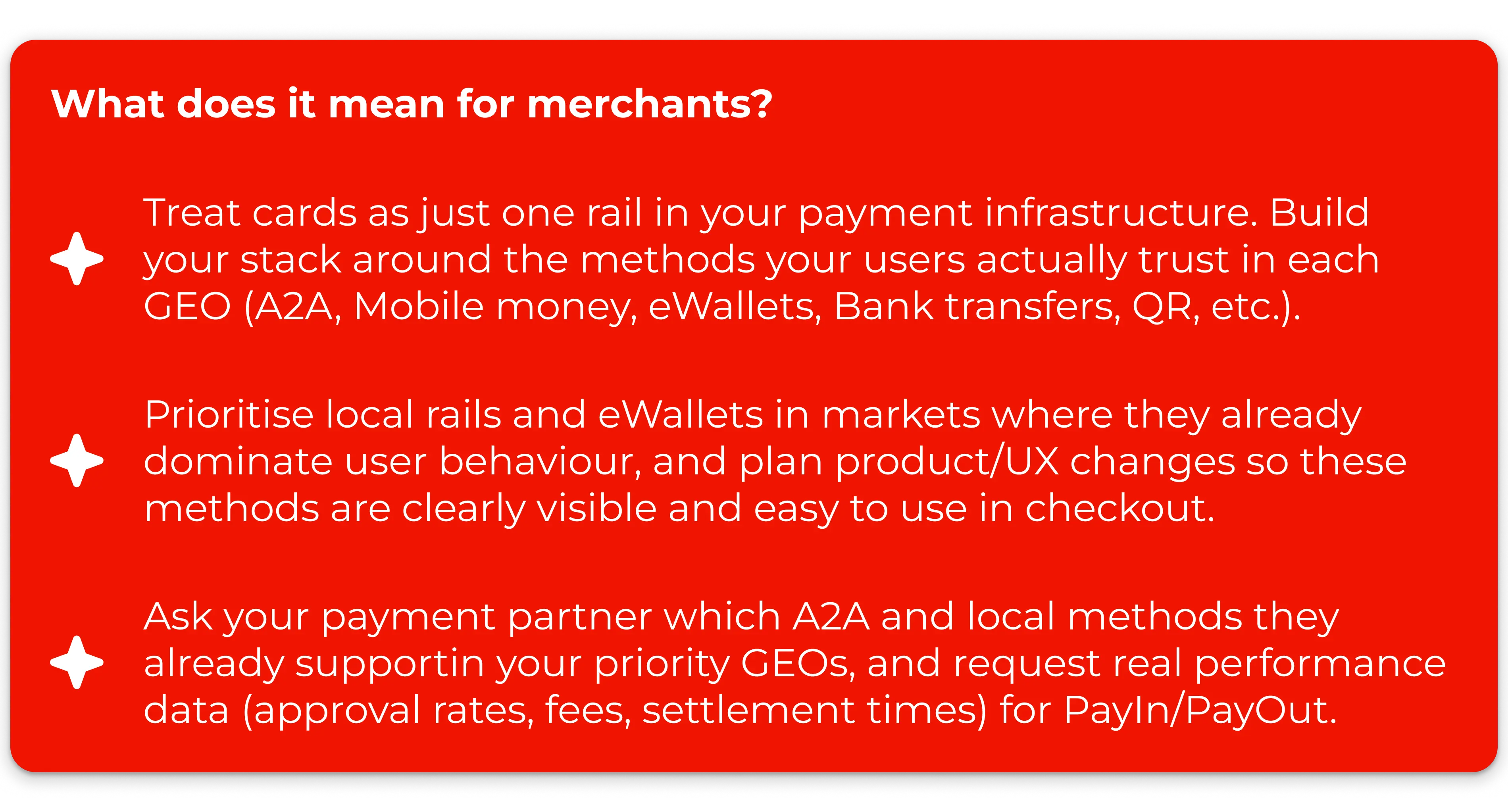

Trend 1: A2A and local rails

Across 2026, card volumes remain important, but most of the incremental growth in Forex, iGaming, and emerging markets comes from Account‑to‑Account (A2A) payments and local real‑time schemes such as UPI, SEPA, and Mobile money networks. Analysts expect A2A volumes and instant transfers to grow rapidly as banks, regulators, and payment providers push lower‑cost, real‑time rails into mainstream use.

At the same time, mobile wallets and super‑apps dominate in key emerging markets: Mobile money in Africa and eWallets in South‑East Asia have become default funding methods for everyday users rather than “alternative” options. The structural shift is that cards are no longer the main growth driver — local rails and wallets are.

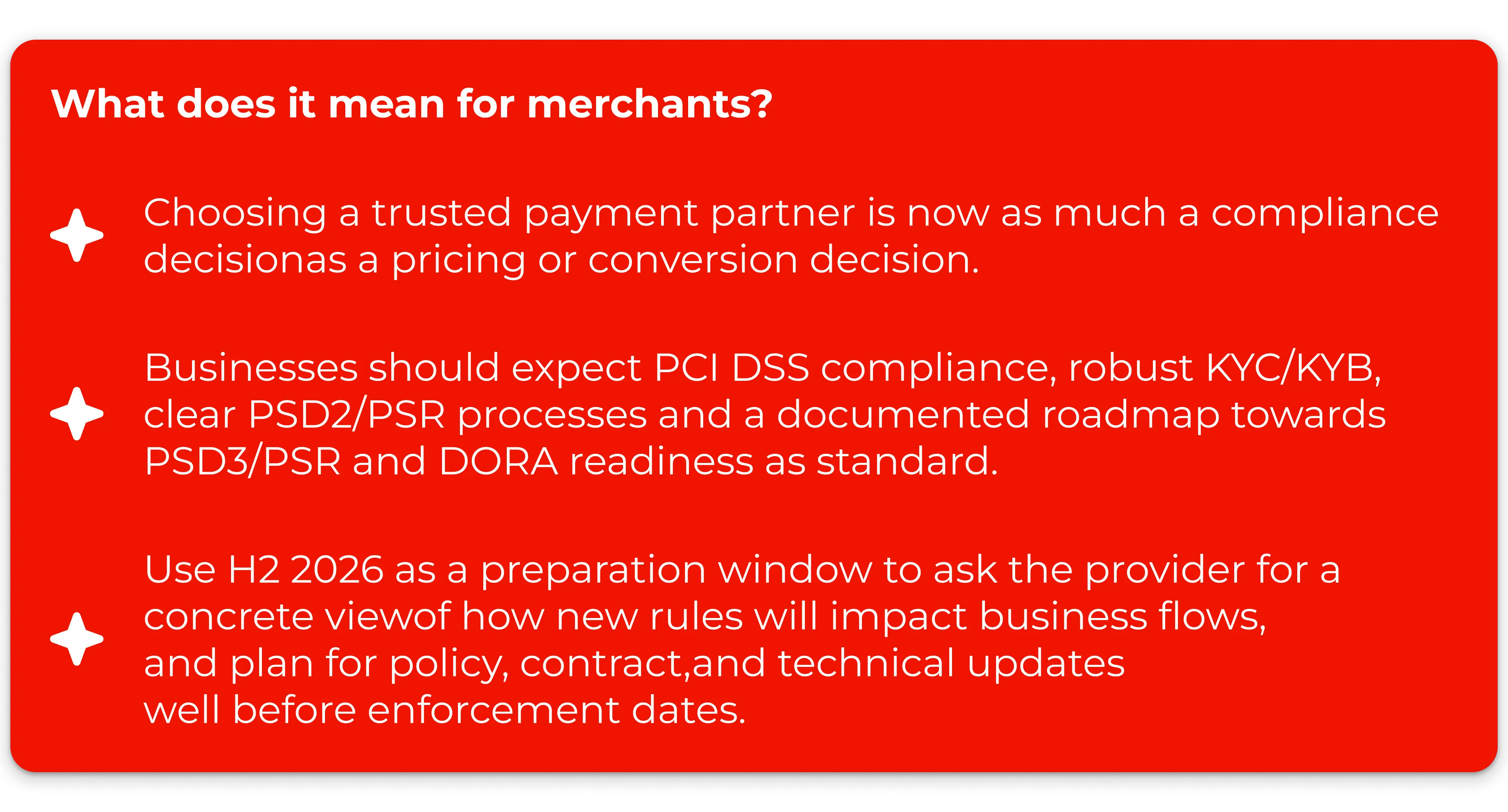

Trend 2: PSD3, DORA, and local rules

H2 2026 is a transition phase for PSD3, the new Payment Services Regulation (PSR) in Europe, and the Digital Operational Resilience Act (DORA). Together, these measures tighten requirements around:

- strong customer authentication and payee verification (including mandatory IBAN–name checks);

- liability and handling of authorised push payment (APP) fraud;

- continuous monitoring of transactions, uptime, and operational resilience for payment infrastructures.

At the same time, High‑Risk processing in regions such as Africa and Asia is increasingly tied to local licensing, domestic regulation and stricter AML/KYC expectations. The underlying change is that payment regulation is becoming more prescriptive and more consistent across markets, with PSPs expected to carry a larger share of compliance and fraud risk.

Trend 3: Localisation and merchant support

Surveys and industry reports show that high‑growth merchants often struggle with providers that lack local presence, have inconsistent uptime, or cannot support their growth plans in new markets. At the same time, expectations for merchant support are rising: 24/7 access, clear SLAs, proactive incident handling, and strategic input are becoming a baseline.

The real shift is that payments teams now expect a partner who helps them interpret data, navigate local regulations, and test new GEOs — not just an API, a dashboard and a generic support inbox.

How to use trends when choosing a payment partner

Bringing these 3 trends together gives a simple checklist when evaluating any high‑growth payment partner in H2 2026:

- Rails & methods

Prove if they support A2A, eWallets, Mobile money, or any local schemes in target GEOs. - Compliance posture

Learn how they prepare for PSD3 and DORA, and which licences they hold in each key region. - Merchant support

Ask about merchant support: what it looks like in practice: response times, channels, escalation paths, and strategic input.

Where SPAYZ.io fits in

If you are reviewing a business’s payment infrastructure for H2 2026 and beyond, SPAYZ.io is exactly this kind of long‑term High‑Risk payment partner. The team focuses on high‑growth sectors such as Forex and iGaming, operates across 35+ GEOs in MENA, Asia, and Africa, and combines local payment methods, robust fraud tools, and 24/7 human merchant support into a single integrated stack.

To explore how these trends apply to your specific markets and payment flows, you can reach out to SPAYZ.io for a tailored review of your current setup.