Settlement is where processed volume becomes usable cash. In High-Risk payments, that stage deserves as much scrutiny as approval rates or coverage, because cycle length, reserve logic and payout costs directly affect liquidity, reconciliation and margin quality.

For merchants in sectors such as iGaming, Forex, and other High-Risk verticals, settlement is the commercial framework in the payment chain that determines when funds are released, what deductions apply before release, and how much operational friction sits between a successful customer payment and the merchant’s working capital.

Settlement in practice

A payment is not fully monetised when it is authorised. In most payment flows, the transaction moves through authorisation, clearing and settlement, with settlement marking the point at which the merchant receives funds under the agreed payout model.

In standard e-commerce, that process may be relatively routine. In High-Risk processing, it is more conditional.

Providers usually assess chargeback exposure, fraud patterns, merchant history, GEO mix, payment method behaviour and compliance risk before deciding how quickly funds can be released and whether any reserves or holdbacks should apply.

That is why settlement should be viewed as a risk-adjusted release process rather than a simple transfer of money. Two merchants can process similar volumes and still have very different settlement terms if their risk profiles, traffic quality, or corridor mixes differ.

How does the settlement cycle work

The settlement cycle is usually expressed as T+n. In many payment environments, settlement typically takes 1 to 3 business days, but High-Risk merchants may start on longer cycles while the processor validates performance and monitors downstream risk.

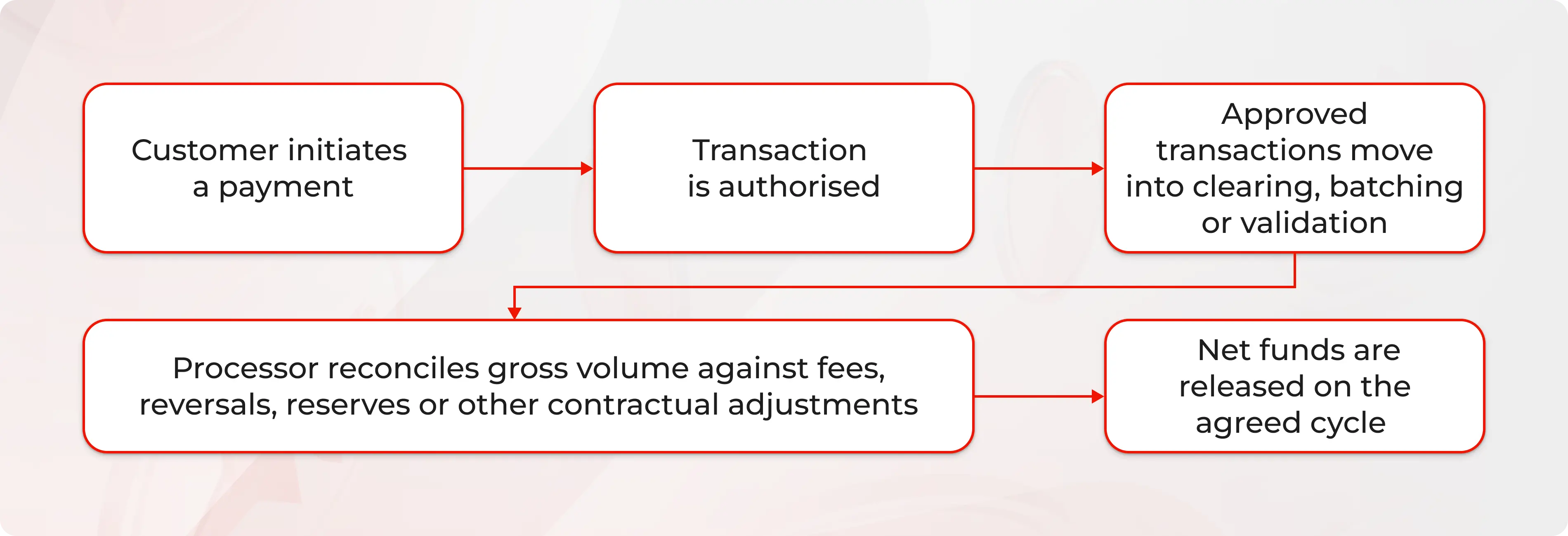

A simplified model looks like this:

For merchants, the key point is that settlement happens on the net amount, not the gross amount processed. This is where reserve deductions, PayOut rules, timing conditions and fee policy start to matter commercially.

Why do High-Risk merchants often wait longer

Longer settlement cycles in High-Risk payments are usually a function of exposure management rather than operational inefficiency. A processor may need time to assess transaction quality, absorb funding pressure, monitor fraud indicators or manage corridor-specific liquidity before releasing funds.

This is particularly relevant for newly onboarded merchants or new local payment corridors. At SPAYZ.io, we note that enabling a new payment partner without committed merchant volume can result in a T+7 settlement cycle in some African markets, which reflects a more cautious early-stage release model.

The same case also shows that settlement is not fixed forever. The combination of local expertise, stronger operator selection, and deeper liquidity support can enable T+1/T+3 settlement in Kenya, illustrating how cycle length depends on infrastructure and confidence in the payment flow rather than on headline promises alone.

Settlement fees and the real commercial impact

Many merchants pay close attention to processing fees but underestimate settlement fees. That is a blind spot because settlement fees are charged when accepted transactions become available for funds, so they directly affect net cash conversion.

Depending on the provider model, settlement fees may be fixed per PayOut, percentage-based, corridor-specific, or embedded in a broader PayOut structure. Even when the fee looks small, the cumulative effect can be material for merchants settling daily, operating across multiple entities or relying on frequent PayOuts to support withdrawals and supplier obligations.

What merchants should ask before signing

Settlement terms should be reviewed as carefully as pricing or approval rates. A merchant should understand not only how fast funds are paid out, but also what can delay release, what deductions apply before payout, and how those movements appear in reporting.

At minimum, merchants should clarify the following points:

- What is the exact settlement cycle by payment method and GEO: T+1, T+2, T+5, T+7 or variable?

- Do weekends and bank holidays affect release timing?

- Are reserves, holdbacks or rolling reserve structures part of the commercial model?

- Is there any explicit settlement fee or payout fee?

- Under what conditions can the cycle be shortened or extended?

- How are deductions, reserve movements and net settled amounts shown in reporting?

These questions help separate a genuinely strong processing setup from one that looks attractive at the front end but creates friction once funds are due to the merchant.

Visibility and speed for settlement

Fast settlement is useful only if it is transparent. Finance and operations teams need to reconcile gross processed volume, failed transactions, reserve movements, PayOut dates and net settled amounts without manual reconstruction.

Our High-Risk processing guidance highlights centralised visibility and operational control as part of a mature payment stack, which is consistent with the needs of merchants managing multiple methods, geographies and provider relationships.

In practice, this means a good settlement model should not only release funds efficiently but also make the release logic intelligible. If a merchant cannot explain why a PayOut amount changed or why a release was delayed, settlement becomes a finance risk in its own right.

SPAYZ.io example

A useful way to frame settlement for merchants is through localisation. SPAYZ.io’s Kenya example shows that the same merchant objective, faster access to funds, can produce different outcomes depending on the maturity of local rails, liquidity support and operator quality. Without committed volume and corridor confidence, settlement may sit at T+7; with the right local infrastructure, the cycle can move to T+1.

That makes the broader point clearly. Settlement speed is rarely an isolated feature. It is usually the result of risk controls, funding capacity, local market knowledge, and operational discipline working together.

What do we have in the end

Settlement in High-Risk payments is the point at which payment performance becomes financial reality, making cycle length, reserve structure, fee policy, and reporting quality central to the merchant’s economics.

For that reason, merchants should assess settlement processing as a full operating model rather than a single PayOut promise. Clear logic, predictable release terms, and the absence of a settlement fee collectively create a meaningful commercial advantage by improving liquidity without adding friction.

If you seek a payment provider that can support your business expansion and offer the most compatible settlement, contact the SPAYZ.io manager to get the best conditions right now.