When merchants expand across regions, one payment stack rarely works everywhere. In High-Risk payments, local payment methods shape approval rates, settlement cycle, settlement fees, fraud exposure, and even whether a market is commercially viable in the first place.

Why do payment methods vary so much by country?

Payment behaviour is local before it is global. Even when international card schemes are available, customers often prefer domestic Bank transfers, eWallets, QR-based systems, or Mobile money because those rails are more familiar, more widely accepted, and often better aligned with local banking habits.

For merchants, this means the question is no longer whether local payment methods matter, but which ones matter in each market. That is especially true in High-Risk verticals, where conversion, PayOut speed, and compliance pressure all depend on choosing the right mix of rails rather than forcing every transaction through one global model.

What matters most for High-Risk merchants?

The settlement cycle matters because slower access to funds creates pressure on cash flow and treasury management. Settlement fees matter because the cheapest nominal route is not always the most efficient one once approval rates, fraud controls, cross-border friction, and operational overhead are taken into account.

USDT settlement has also become part of the discussion in High-Risk fintech because some merchants need faster cross-border treasury movement and more flexible settlement options. However, stablecoin settlement still requires clear governance around AML, KYC, eWallets, and legal treatment in each operating market.

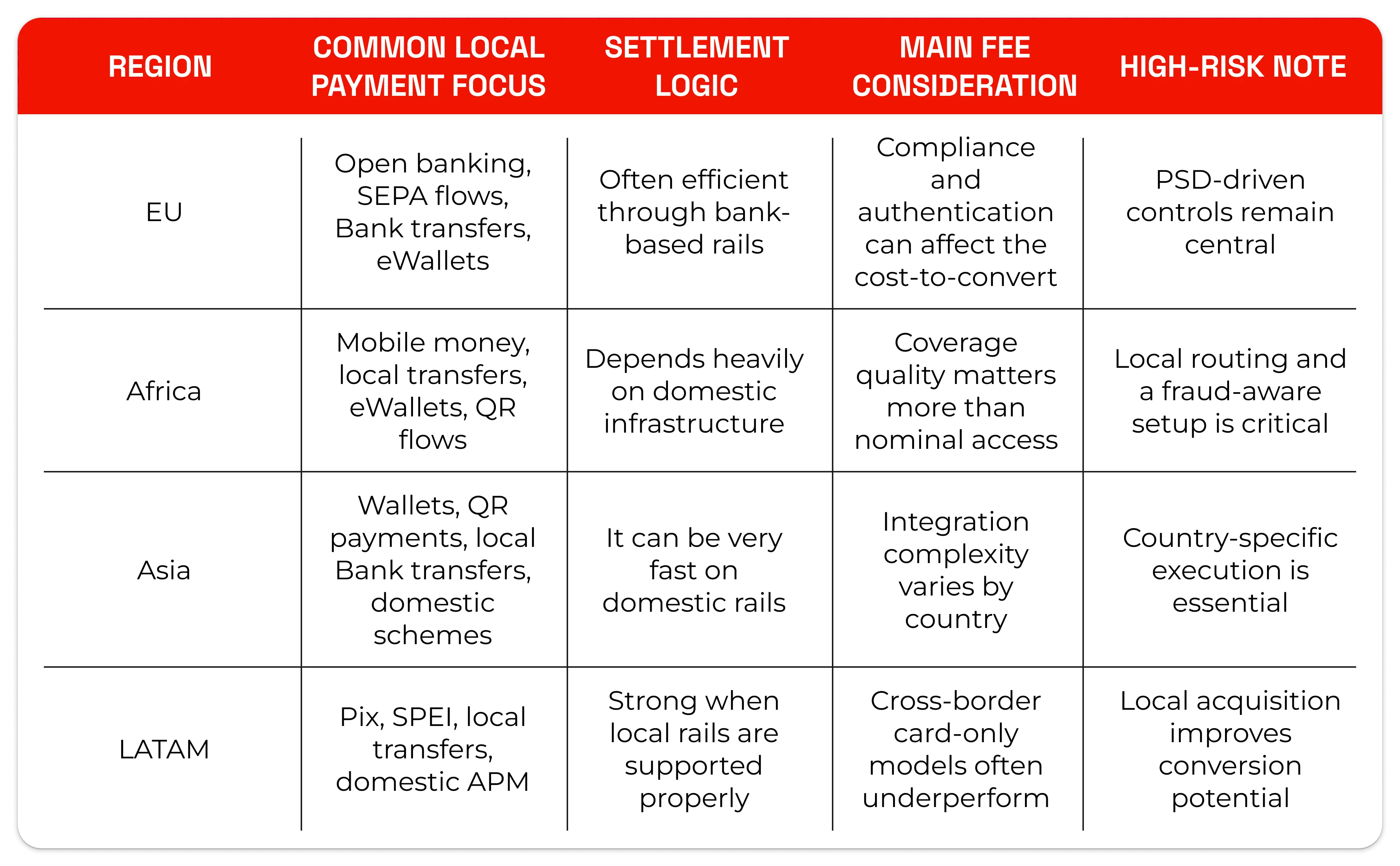

Payment methods in Europe

In Europe, the most commercially important methods tend to include Bank transfers, SEPA-linked flows, Open banking, local card schemes, and eWallets. For many merchants, especially in regulated or high-friction sectors, account-to-account and bank-based payment flows can reduce unnecessary friction compared with relying only on international cards.

The European market is often perceived as mature, but it is not uniform. Merchant performance still varies by country because issuer behaviour, authentication requirements, compliance expectations, and customer checkout habits differ across the region.

From a settlement perspective, Europe is attractive because Bank-based and Open banking rails can support relatively efficient fund movement, especially when compared with more fragmented cross-border card setups. From a risk perspective, however, merchants still need to design around PSD-driven compliance, fraud prevention, and strong customer authentication requirements.

Payment methods in Africa

In Africa, local payment methods are often built around mobile-first behaviour. Mobile money, domestic Bank transfers, eWallets, QR-enabled flows, and country-specific alternative payment methods can be more relevant than international card acceptance in a day-to-day conversion strategy.

That is why Africa should not be treated as a single card market with coverage gaps. In many countries, payment success depends on understanding domestic infrastructure and routing customers towards methods they already use for everyday transfers and bill payments.

For High-Risk merchants, the operational lesson is clear: local relevance usually matters more than brand familiarity. A provider with real regional coverage, local settlement capabilities, and fraud-aware routing is usually better positioned than a global acquirer that offers nominal access but weak local performance.

Payment methods in Asia

Asia is one of the clearest examples of why a country-by-country payment strategy matters. The region includes major wallet ecosystems, instant Bank transfer rails, QR payment cultures, domestic card networks, and bank-driven methods such as UPI and other local transfer models.

In practice, merchants entering Asia often discover that customers are willing to pay, but not necessarily through the methods that work in Europe or North America. Approval rates and checkout completion improve when the payment stack reflects local habits rather than trying to standardise them away.

The settlement cycle in Asia can be highly competitive, where instant or near-instant domestic rails are well established. At the same time, operational complexity remains high because each country has its own mix of banking rules, preferred methods, fraud patterns, and integration standards.

Payment methods in LATAM

LATAM is now one of the most important regions for merchants looking at local payment methods because consumer behaviour is strongly shaped by domestic rails. Public guidance on the region highlights methods such as Pix in Brazil, SPEI in Mexico, local Bank transfers, Crypto, and domestic alternative payment methods that are often better suited to local commerce than international card-only approaches.

This matters because many local cards and payment methods in Latin America are primarily designed for domestic use. As a result, merchants that treat LATAM as a standard cross-border card market often see unnecessary friction, higher decline rates, and lower conversion than merchants that localise properly.

For High-Risk sectors, LATAM can be commercially strong when the provider supports local acquiring, regional routing, and settlement logic that reflects domestic payment behaviour. Without that infrastructure, even a well-marketed product can struggle at the final step of the customer journey.

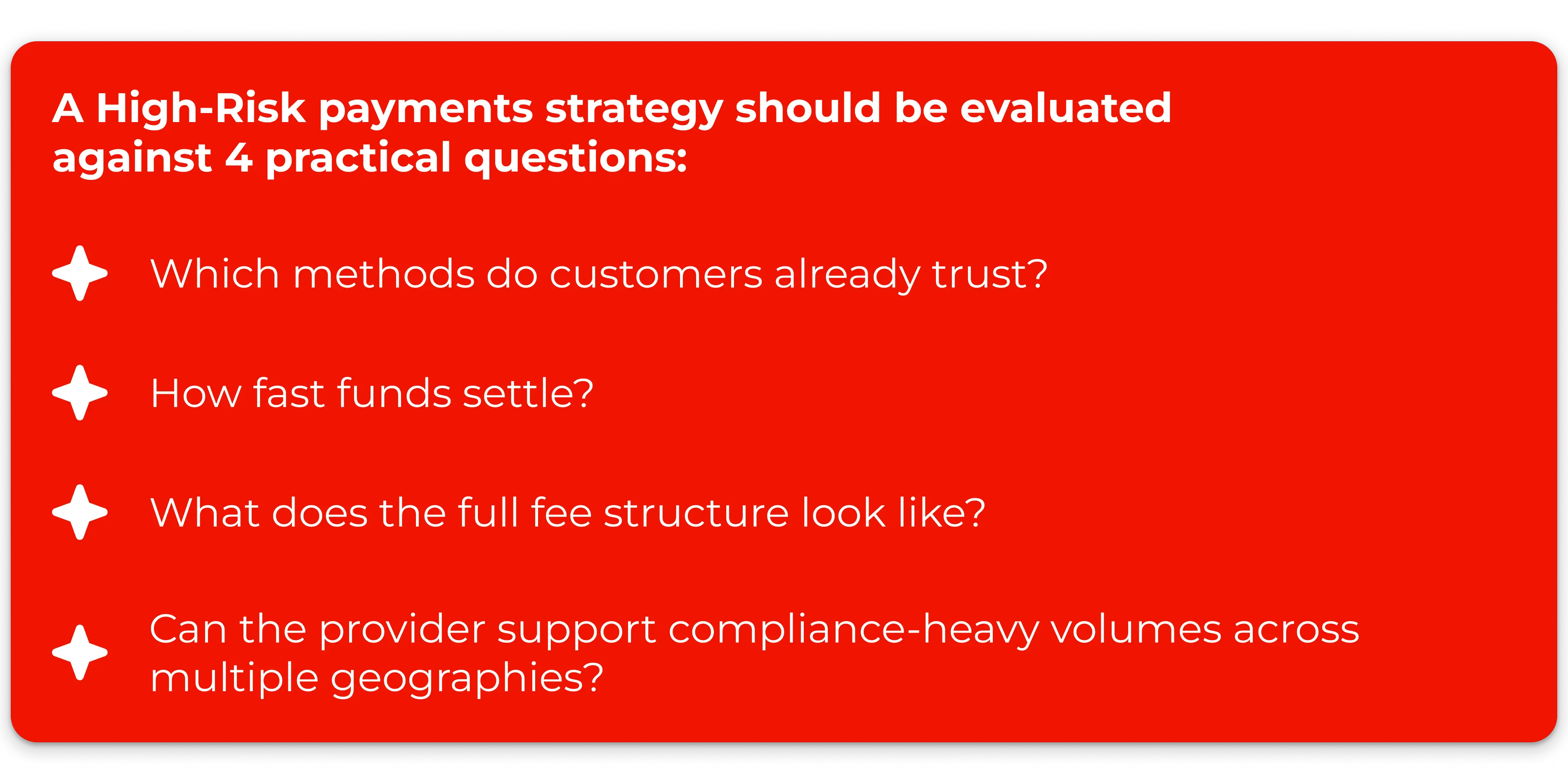

What is the best way to choose payment methods by country?

A practical market-entry model should prioritise local behaviours over global preferences. Merchants ought to evaluate each target country based on 4 criteria:

- customer payment habits

- the expected settlement cycle

- the total fee burden

- the provider’s capability to support compliance and manage fraud at scale

The best payment stack isn't always the one with the longest list of options. Instead, it's the one that truly aligns with local user habits, offers a sensible settlement cycle, maintains sustainable fees, and allows merchants to thrive even in High-Risk environments.

At SPAYZ.io, we’re excited to expand and support regions across Asia and Africa with a range of local payment methods, Bank transfers, eWallets, QR payments, Mobile money, and tailored settlement solutions for High-Risk merchants. If you’re looking to boost conversions, reduce friction, and explore new markets through a payment stack that meets local needs, now is the perfect time to connect!