High-risk payment processing in industries like iGaming, Forex, and crypto is limited by three factors: low approval rates, high chargebacks, and unstable payment flows across GEOs. Most PSPs try to solve these issues separately. But in practice, they are interconnected.

This guide reveals SPAYZ.io’s 5 main principles, backed by real-world cases, metrics, and actionable tips to help you outperform competitors.

Principe 1: Payment routing must adapt in real time

One of the main reasons for failed transactions in high-risk payments is incorrect routing. Intelligent routing directs transactions through optimal paths, minimising declines in high-risk environments. Instead of sending all traffic through a single provider, the system distributes transactions based on:

- GEO and currency

- payment method availability

- historical approval rates per provider

For example, in Asia, shifting traffic to local payment channels such as UPI and IMPS, rather than relying on international gateways, significantly improved transaction performance. Approval rates increased from around 70% to over 90%, primarily due to lower latency and better alignment with local banking infrastructure.

A similar pattern can be observed in iGaming markets across Africa. Routing transactions through Mobile Money solutions in countries such as Nigeria and Tanzania not only improved acceptance rates but also reduced chargebacks by 30–35%. At the same time, this setup supported the seamless processing of high transaction volumes on an annual scale, without adding operational complexity.

Key idea: approval rate optimisation starts with routing logic depending on local solutions.

Principe 2: KYB should filter risk before transactions start

Know Your Business (KYB) verifies merchant legitimacy, essential for high-risk PSP survival amid tightening regs. Many issues that appear later, including fraud, disputes, and unstable transaction flows, often originate at the onboarding stage. This is why KYB should not be treated as a formal compliance step, but as an early risk-filtering mechanism.

A structured KYB process includes:

- verification of UBOs and licenses

- transaction pattern analysis during onboarding

- continuous monitoring after approval

For example, in crypto onboarding, this approach enabled the identification of up to 15% of potentially high-risk profiles before they became active. As a result, fewer problematic transactions entered the system in the first place, which directly reduced future chargebacks and operational load. In practice, this also leads to faster, more predictable onboarding, since low-risk merchants pass verification without delay.

Principe 3: Local payment methods define conversion

Performance in high-risk payments is highly dependent on geography, as user behaviour, payment preferences, and banking infrastructure vary significantly between regions. A setup that works in Europe may underperform in Asia or Africa if it relies on the same payment methods and routing logic.

- Mobile Money in Africa significantly reduces chargebacks compared to card payments

- Local bank rails in Asia improve approval rates due to lower latency and higher trust

Effective GEO optimisation requires adapting the payment stack to each region. This includes integrating local payment methods such as eWallets, QR-based systems, bank transfers, and Mobile Money, as well as supporting local currencies and settlement flows. These adjustments reduce friction at the payment stage and increase trust from end users.

Key idea: GEO expansion works only when payment methods match user behaviour.

Principe 4: Fraud prevention must work during the transaction

In high-risk environments, reacting to fraud after a transaction is often too late. By that point, funds may already be disputed, and recovery becomes costly and uncertain. This is why fraud prevention needs to be embedded directly into the payment flow.

A practical approach combines real-time transaction scoring, conditional 3D Secure, and behavioural analysis. Each transaction is evaluated dynamically based on multiple signals, including user behaviour, transaction patterns, and historical data. Instead of applying rigid rules, the system adjusts the level of verification depending on the risk level of each payment.

Principe 5: P2P infrastructure needs centralised control

P2P models are widely used in high-risk payments, particularly in regions where traditional acquiring is limited. However, without proper infrastructure, managing agent networks quickly becomes inefficient. Manual tracking, fragmented data, and delayed reconciliation create operational bottlenecks and increase the risk of errors.

SPAYZ.io offers a centralised P2P Agent Dashboard that addresses these issues by bringing all operations into a single interface. Dashboard allows:

- Track all your transactions in real time

- Control agent activity management across multiple GEOs

- Automate reconciliation processes

This resulted in faster payout cycles and more stable transaction handling. The main benefits are efficiency and the ability to scale high-risk operations without losing control of the process.

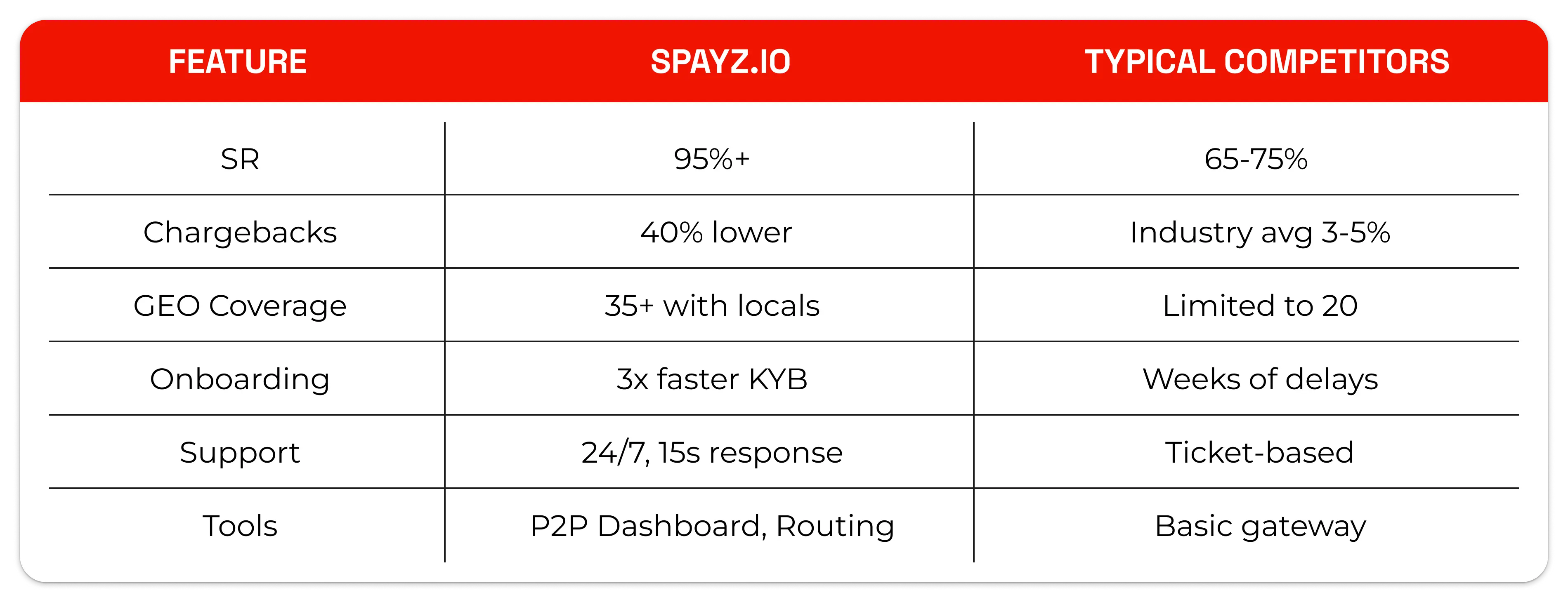

How SPAYZ outperforms competitors

Key takeaways

High-risk payment processing can’t be stabilised with a single tool or isolated fix. Approval rates, chargebacks, and scalability are interconnected, and each depends on how well the entire system is structured. When all elements are aligned, payment performance becomes predictable, even in volatile markets.

This is exactly where SPAYZ.io comes in to support high-risk businesses. By combining routing logic, structured KYB, GEO-specific optimisation, and real-time fraud control into a single, scalable system. Instead of solving issues one by one, this approach addresses the entire payment flow.

If you are looking to improve approval rates, reduce chargebacks, or expand into new GEOs, contact us to analyse your business processes and pick up the best personalised solution.