In Forex, iGaming, and other High-Risk verticals, payment success rate (SR) is not just an operational KPI; it is a direct measure of how well the payments stack fits a specific market. Approval rates vary significantly across the EU, LATAM, Africa, and Asia because they are shaped by local payment habits, issuer policies, compliance requirements, routing quality and the availability of local acquiring.

For product teams and payment managers, that distinction matters. The same checkout can deliver very different conversion rates across GEOs, even when the product, offer, and traffic quality remain unchanged, which is why regional payment performance should be analysed in the context of individual countries, payment methods, and use cases rather than as a single blended average.

Why can the approval rate not be compared at face value

When businesses look at average payment approval rates by region, it is tempting to seek a single benchmark for Europe, Latin America, Africa, or Asia. In practice, approval rates by country are shaped not only by the PSP but also by a combination of local payment methods, issuer behaviour, compliance controls, fraud pressure, and the quality of fallback routing.

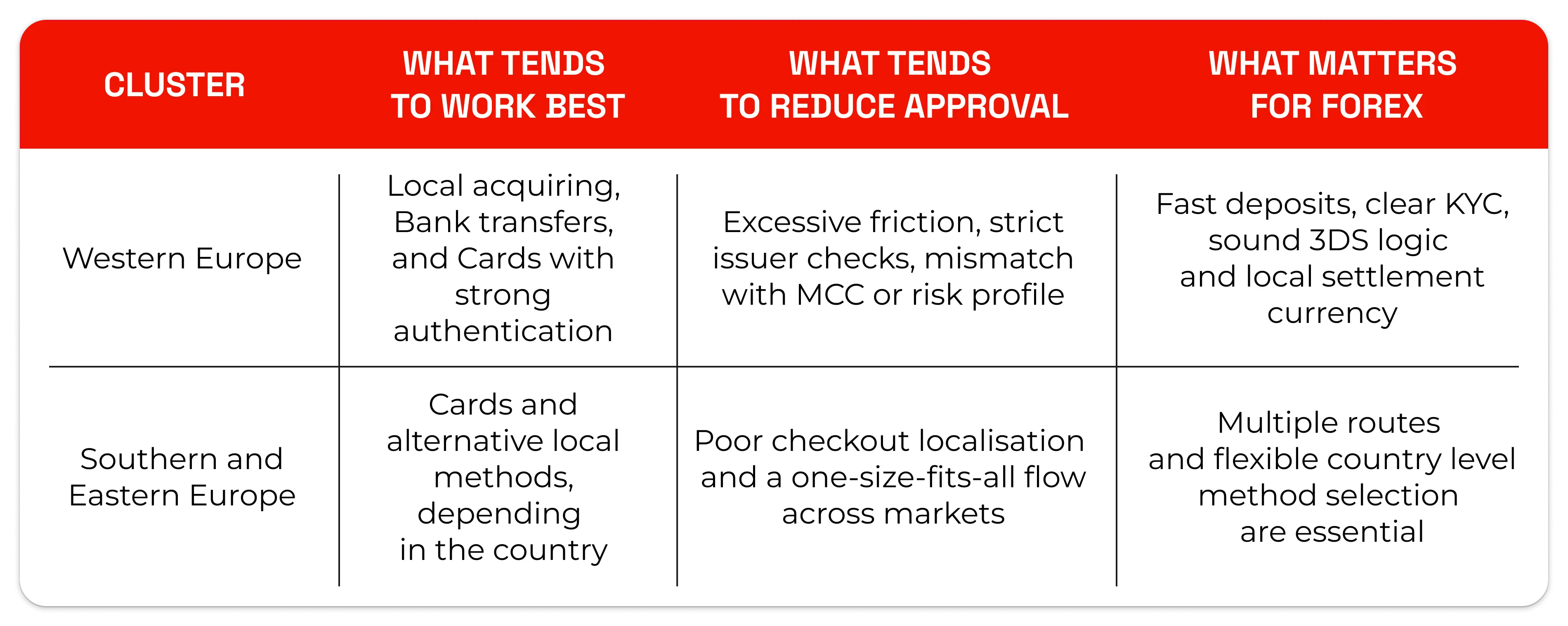

EU: stable infrastructure, stricter compliance

Europe is generally the most predictable region from a payments perspective. Local infrastructure is mature, Bank transfers and cards are deeply embedded in customer behaviour, and the regulatory environment creates a more standardised operating model than many other markets.

That said, a mature market does not automatically mean a high payment success rate across all verticals. For Forex and other High-Risk businesses, Europe remains a region where compliance burdens and issuer policies can materially affect approval: the higher the perceived risk, the more likely a transaction is to fail, even if it is technically valid.

Local payment preferences also matter in Europe. In some countries, Bank transfers perform better; in others, Cards or Mobile wallets are the better fit.

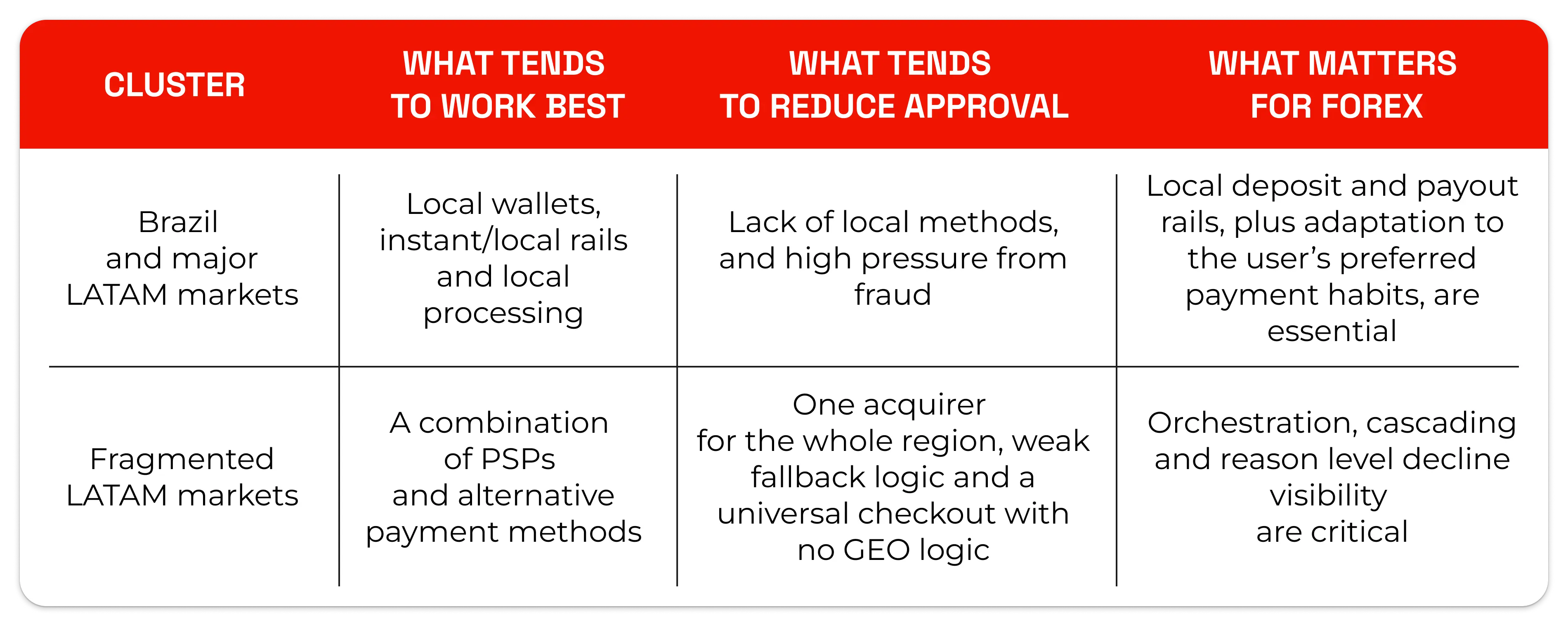

LATAM: strong local specificity and higher fraud sensitivity

Latin America usually shows a much more fragmented approval picture by country. Even neighbouring markets can differ in their reliance on cash alternatives, local wallet solutions, Bank transfers and the extent to which they trust international card rails.

One reason the payment success rate is often lower in LATAM is the fragmented payments environment. The market is influenced by a large number of local providers, uneven banking digitalisation, issuer policy volatility and stronger fraud sensitivity, which means an unlocalised flow often produces far more declines than it would in Europe.

For Forex, this is crucial because users expect a fast deposit with as few steps as possible. If the provider doesn’t support familiar local methods or tries to route payments through offshore and irrelevant rails, the business loses not only the transaction but often the customer at the first funding attempt.

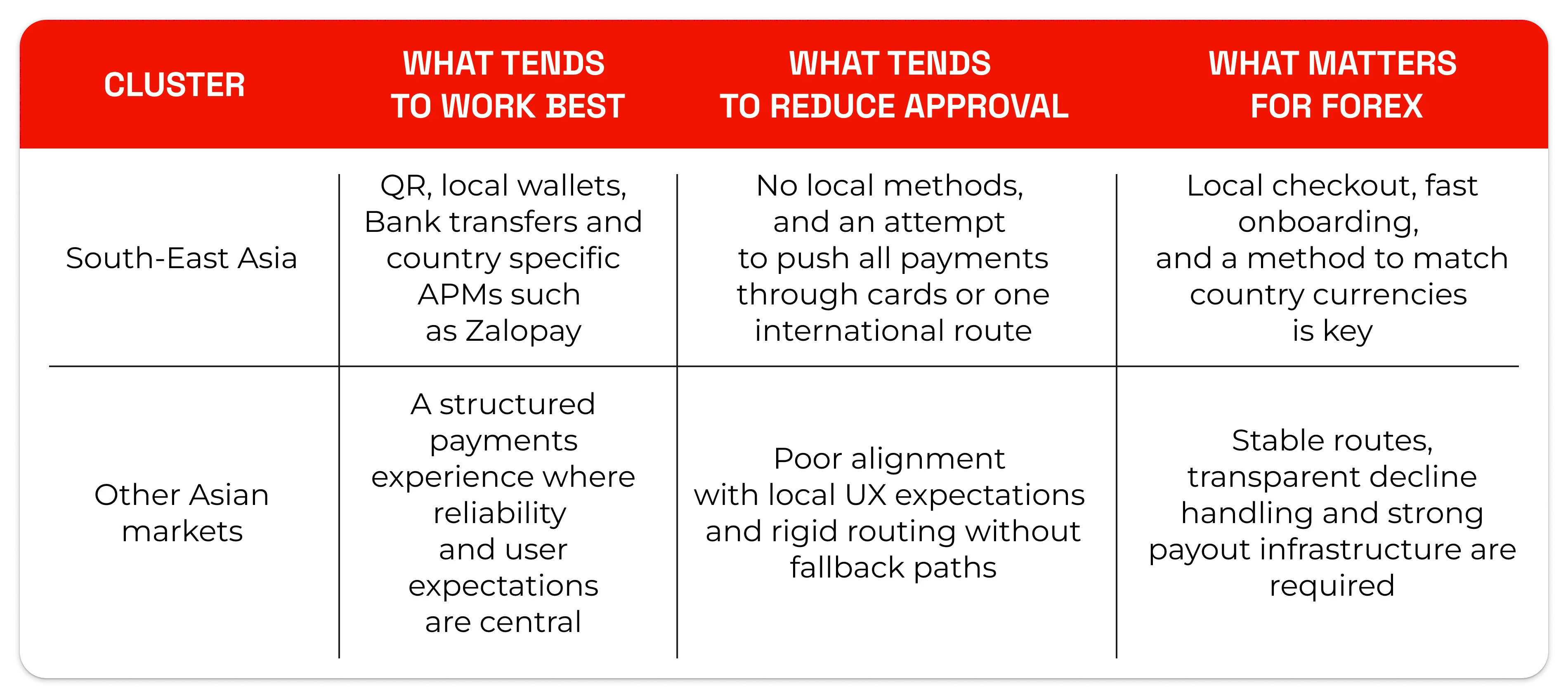

Asia: local methods matter more than provider brand

Asia is the region where local payment performance depends most strongly on individual countries and their local payment habits. This is where average payment approval rates by region become useful as a broad headline metric, but too general for product decisions: actual results are driven by how well a PSP supports local rails and the specific customer journey in each market.

In parts of Asia, local APMs, Bank transfers, QR payments and wallet-based models matter more than international cards. In High-Risk verticals, that means even a technically strong global provider can underperform on payment success rate if it doesn’t support the right methods, currencies and fallback routes.

In Forex scenarios, localisation is particularly important for first deposits and withdrawals. When users expect instant Bank transfer, local wallet, or P2P mechanics, forcing them into a card-only route can significantly reduce approval rates and damage the overall customer experience.

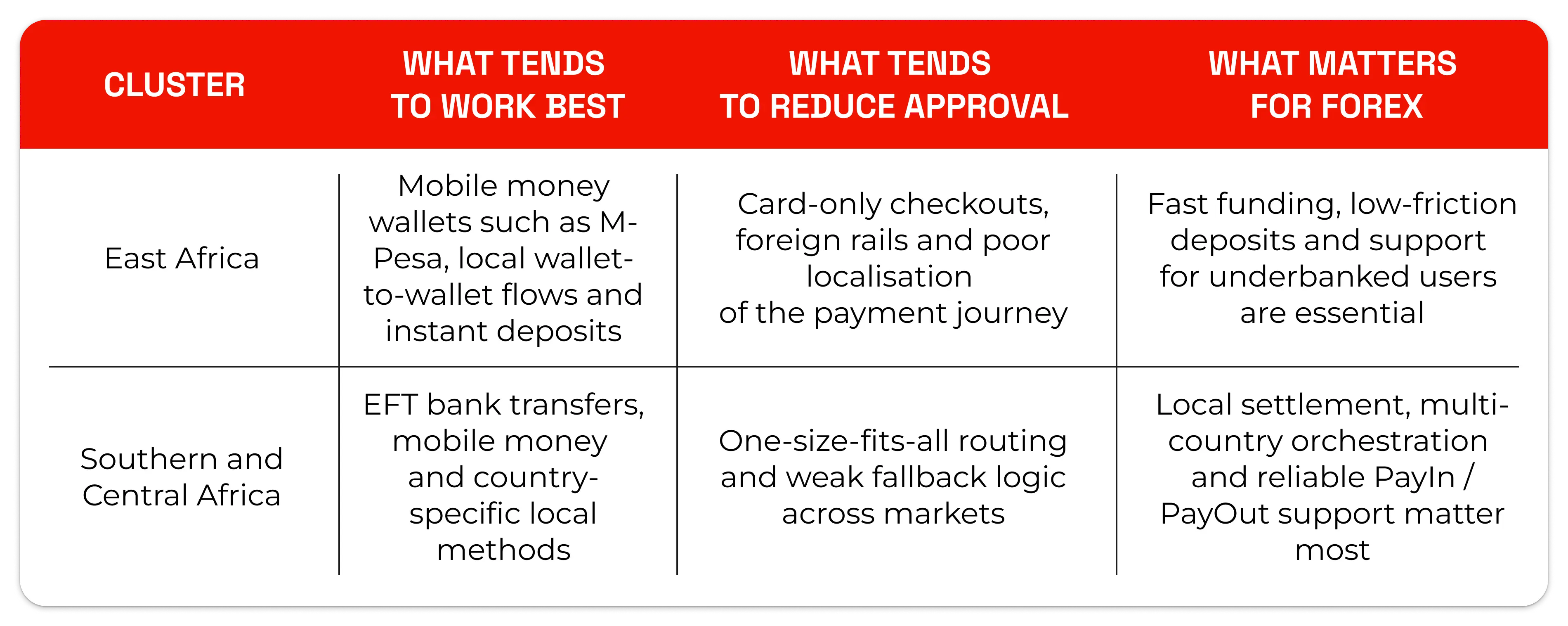

Africa: mobile money and local rails drive approval

Africa is a market where payment success rate is driven far more by mobile money, local Bank transfers and real-time rails than by traditional card processing. In many countries, the most reliable path to higher approval is not to push customers into international card flows, but to support the local payment habits they already use every day for deposits, peer-to-peer transfers and bill payments.

For High-Risk sectors such as Forex, that distinction is especially important. Regional payment performance depends on whether the provider can match the country-specific payment behaviour of each market, including Mobile wallets, Bank transfer rails and instant payment systems that feel familiar, fast and low-friction to the end user.

Where local options are unavailable, checkout conversion tends to weaken quickly. Card-only flows, offshore routing and limited fallback logic can all reduce payment success rate, particularly in markets where financial inclusion is still being built through mobile money and where users expect a payment experience designed around local infrastructure rather than imported assumptions.

Why markets perform differently

The first factor is local payment habits: customers in different countries prefer different combinations of Cards, eWallets, Bank transfers and QR payments, so the same checkout can perform very differently from one GEO to another.

The second is issuer behaviour and compliance. Even when the payment method is the same, final approval depends on the bank’s internal rules, the quality of the KYC/AML flow, sensitivity to high-risk verticals, and whether the route matches the transaction's country, currency, and risk profile.

The third is the quality of local acquisition and routing. When the provider can combine local methods, multiple processing routes, and rule-based cascading, it reduces first-attempt losses and improves the payment success rate without aggressive or duplicate retry logic.

What this means for product teams

For a product-led article, the key point is not to promise universal averages where they can’t be measured accurately without internal provider and merchant data. A more professional approach is to explain why country-level approval rates must be analysed alongside the payment-method mix, local regulations, fraud pressure, and orchestration quality, rather than comparing countries on a single metric.

In practice, that means a few clear rules:

- Compare approval not only by region but also by country, method, and whether it's a first or repeat payment.

- Assess payment success rate separately for deposit and payout flows, especially in Forex.

- Check whether the provider offers local rails, fallback routing and visibility into decline reasons.

- Treat checkout localisation as part of the payments strategy, not just as a UX improvement.

SPAYZ for High-Risk markets

For Forex and other High-Risk verticals, SPAYZ.io focuses on what actually moves the needle on approval: 35+ GEOs, a broad set of local methods, support for eWallets, Bank transfers, Mass payouts and QR payments, plus routing infrastructure that can be adapted by market, currency and transaction type.

SPAYZ.io also emphasises compliance-aware processing, PCI DSS, 3-D Secure, 24/7 support, and the operational tools needed to achieve a more resilient payment success rate in complex GEOs and High-Risk segments.

If you are already trying to improve your business, contact SPAYZ.io right now!