PSD3 marks a major evolution from PSD2, introducing stricter rules on fraud prevention, open banking, and compliance that directly impact Forex brokers handling high-risk payments. These changes aim to enhance security and harmonisation across the EU, but they pose challenges for Forex brokers, particularly regarding recurring payments and SEPA requests (SR). Here's a structured overview to help you navigate PSD3 compliance for high-risk Forex operations.

PSD2 vs PSD3: core differences

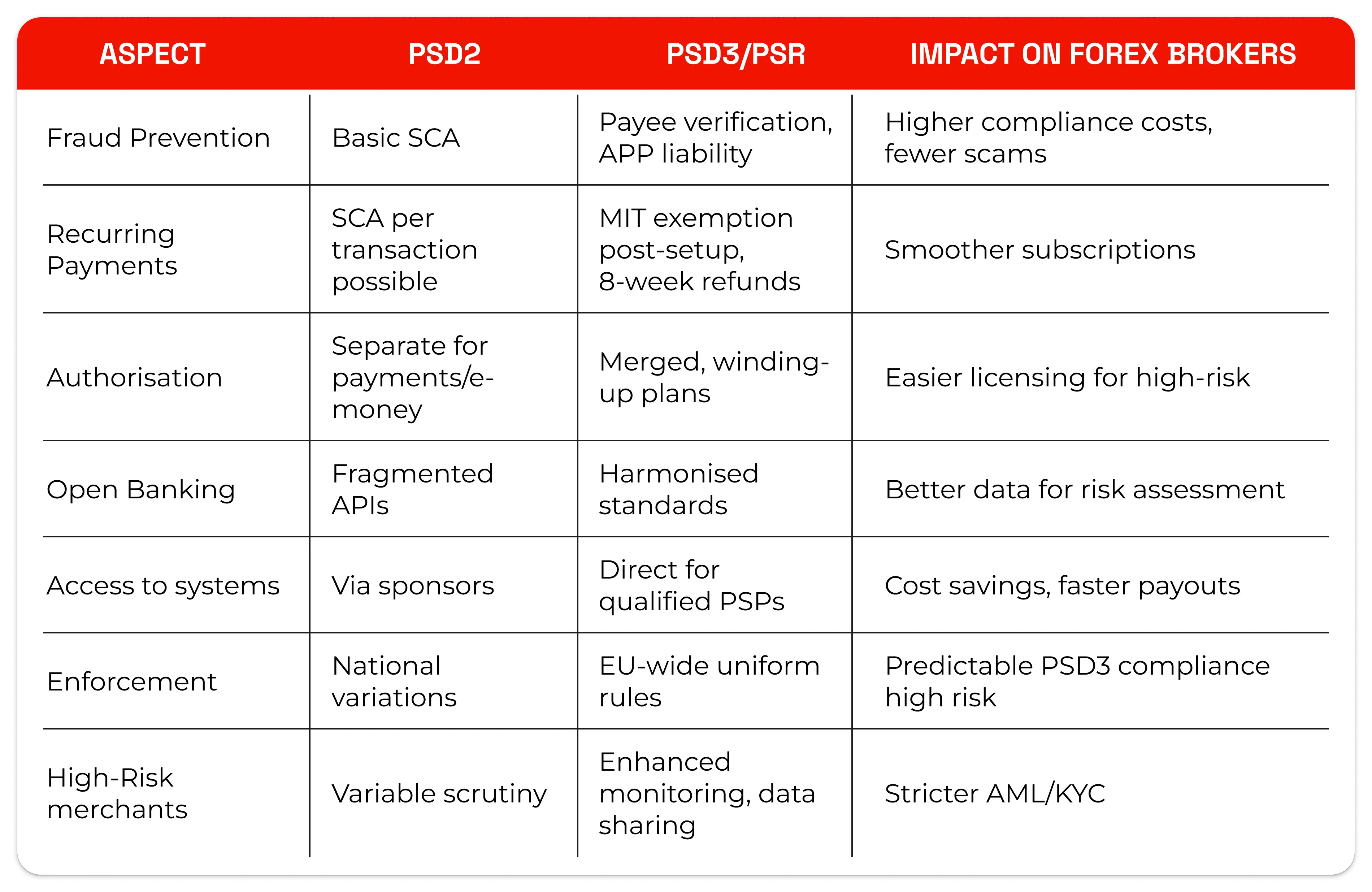

PSD2, effective since 2018, focused on open banking and strong customer authentication (SCA), but it led to fragmented implementation and rising fraud. PSD3, proposed in 2023 and nearing final adoption in 2026, shifts many rules to the directly applicable Payment Services Regulation (PSR) for uniform EU enforcement.

Key upgrades include merged licensing for payment and e-money institutions, direct access to payment systems for non-banks, and broader fraud liability. For Forex brokers, this means tighter oversight on high-risk merchant accounts, affecting payment gateways and cross-border flows.

7 shocking changes impacting Forex brokers

PSD3 brings surprises that could disrupt Forex operations, especially in high-risk EU Forex payment regulation.

1. Mandatory payee verification

All credit transfers now require IBAN-name matching to prevent fraud, shocking brokers reliant on quick SEPA transfers. Mismatches could spike declines, hitting deposit speeds.

2. Expanded fraud liability

Banks and PSPs face liability for authorised push payment (APP) scams, which may extend to Forex platforms if weak verification is proven. Brokers must upgrade anti-fraud tools or risk penalties.

3. Unified authorisation framework

PSD3 repeals PSD2 and EMD2, merging rules for payment institutions—simplifying but demanding winding-up plans and higher capital for high-risk Forex.

4. Direct payment system access

Non-banks like Forex PSPs gain direct SEPA participation, cutting sponsor bank costs but requiring PSD3 compliance high risk setups.

5. Stricter SCA with exemptions

SCA tightens requirements for high-value trades, but MIT exemptions ease the need for recurring Forex deposits after initial authorisation.

6. Open banking overhaul

Harmonised APIs boost data access, aiding Forex KYC but mandating secure third-party sharing.

7. Instant payments mandate

Paired with SEPA Instant rules, PSD3 pushes <10s transfers, challenging Forex brokers' liquidity in the high-risk EU Forex payment regulation.

Comparison Table: PSD2 vs PSD3

PSD3 impact on recurring payments and SR

Recurring payments (subscriptions for Forex signals/tools) and SEPA Requests (SR) are undergoing significant changes. PSD3 exempts merchant-initiated transactions (MIT) from repeated SCA after mandate setup and provides an 8-week refund right, as with SEPA Direct Debits. This smooths Forex recurring deposits but demands robust mandate management to avoid disputes.

For SR, payee verification adds friction but reduces errors in high-volume Forex inflows. Brokers must integrate dynamic recurring payments (DRP) via updated SPAA schemes, boosting conversion but risking non-compliance fines. High-risk Forex brokers see a 20-30% drop in fraud risk, per industry estimates.

PSD3 compliance challenges for High-Risk Forex

Forex brokers, classified as high-risk due to volatility and chargebacks, face amplified PSD3 compliance high-risk demands. Key hurdles: upgraded transaction monitoring, GDPR-aligned data privacy, and PCI DSS compliance for cards.

Non-compliance risks €5M+ fines or license revocation. Cross-border Forex payments get uniform rules, ending "forum shopping" but requiring multi-geo AML.

How Spayz helps Forex brokers migrate to PSD3

Spayz.io, a payment provider for high-risk sectors such as Forex, eases PSD3 migration by already having PSD2-compliant open banking. Their solutions cover EU bank connectivity, eWallets, mass payouts, and acquiring, tailored for Forex PayIn/PayOut.

Recent updates at iFX Cyprus 2025 enhance open banking for PSD3 APIs, ensuring seamless recurring SR and MIT. Spayz handles anti-fraud, 24/7 support, and multi-geo (35+ countries) compliance, reducing migration time by 50% via single API integration. Brokers report 23% higher success rates post-Spayz integration.

PSD3 compliance checklist for Forex brokers

Use this actionable checklist for PSD3 compliance with high-risk Forex payment regulation EU:

- Audit current setup: review SCA, APIs against PSR rules.

- Implement payee checks: Integrate IBAN verification for all SEPA.

- Upgrade fraud tools: add real-time monitoring and behavioural analysis.

- Secure recurring flows: set MIT mandates with refund policies.

- License check: prepare winding-up plan, capital proofs.

- Partner with a compliant PSP, like Spayz, for open banking/mass payouts.

- Test & Train: simulate PSD3 scenarios, staff on new liabilities.

Preparing your Forex business for PSD3

Start migration early to turn PSD3 into a competitive edge: lower fraud, faster payments, better trust. Partnering with Spayz.io ensures PSD3 compliance, mitigates high risk without downtime, and supports Forex growth in the EU and beyond. Contact us for more information.